Why Young Indians Earn More But Feel Financially Stuck

Young Indians financially stuck – this is a scenario more familiar than we care to admit. From a bustling coffee shop in South Delhi, where I often sip my cappuccino and observe the vibrant mix of professionals around, a disturbing theme emerges. Despite earning more than their parents at the same age, many feel a financial anxiety that clouds their well-being. They appear successful but carry invisible burdens on their shoulders. In my experience, young Indians, especially here in Delhi, navigate not just their careers but a complex web of family expectations and societal pressures that seem to consume their earnings before they even touch their wallet. Let’s delve into why, despite high salaries, so many feel they are financially stuck.

Young Indians financially stuck feel their salaries evaporate in the blink of an eye. It seems as though the paycheck arrives only to disappear, leaving behind stress and inquisition. One minute you’re celebrating a new job offer, and the next, your monthly budget is strangling you. What is happening here? The truth lies in uncalculated “expenses” like societal expectations and family commitments, which pull at the seams of every paycheck. Despite what seems like a comfortable salary, young Indians are often surprised at how little they’ve got left to actually save for their own future.

Invisible Charges on Salaries

These invisible charges start with societal expectations that seem to dictate buying a smartphone upgrade annually or dining at the latest restaurant. Every occasion calls for a financial celebration, eroding savings silently. Moreover, unlike salaries in idyllic job descriptions, the real income considering these costs often feels inadequate.

Penny Pinching or Wise Spending?

Whether it’s medical bills or weddings, you’re left wondering if you’re living beyond means or they’re simply beyond control. It’s not about penny-pinching but recalibrating spending habits that realign personal happiness with financial realities. Yet, negotiating this balance is one reason many young Indians are financially stuck.

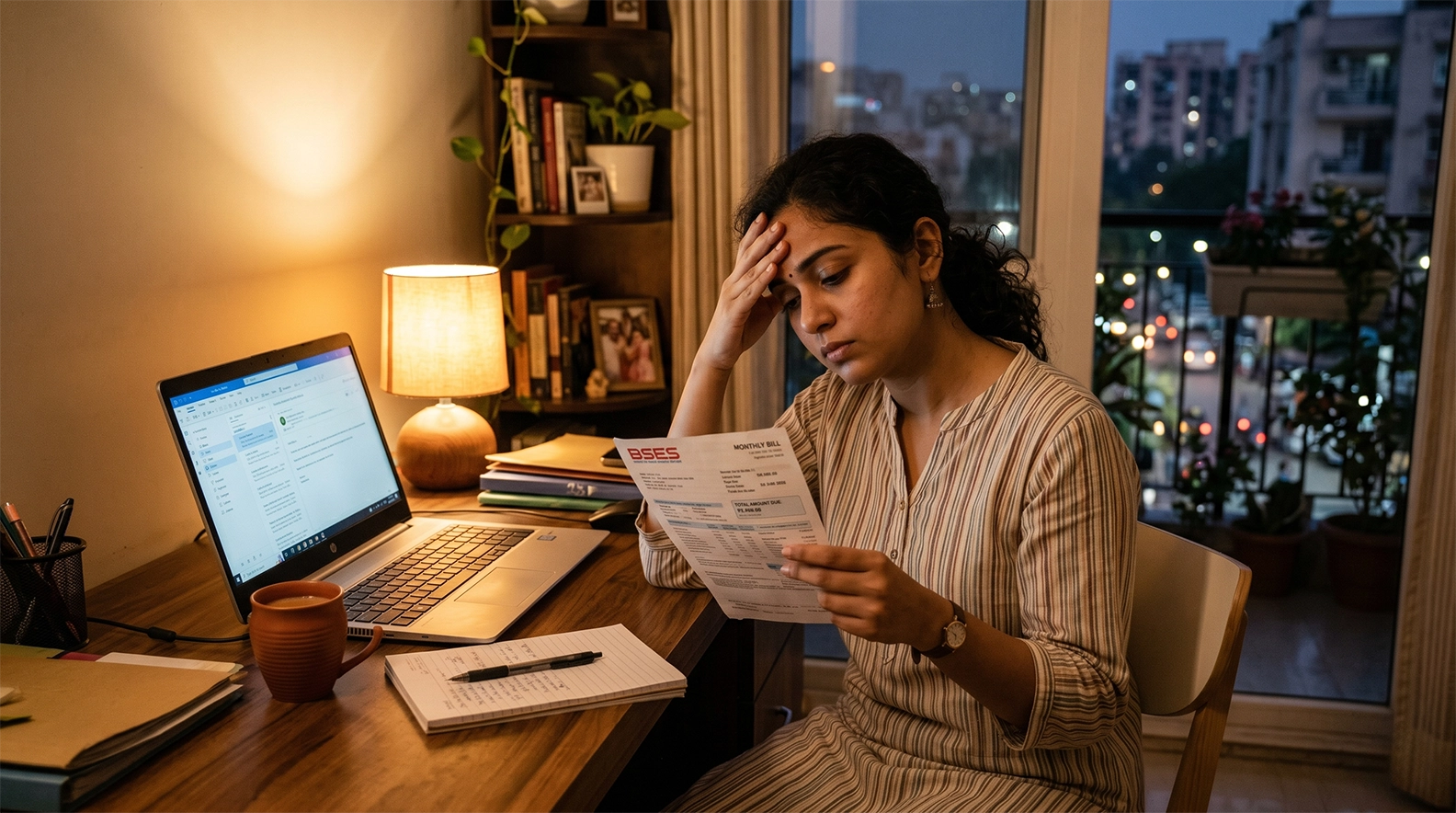

Why NCR Costs More Than Your Payslip Shows

For young Indians financially stuck, Delhi’s cost of living can be a harsh realization. The capital’s bustling life comes with a steep price tag, from the soaring rents to expensive leisure activities. When we factor in inflation, it’s no surprise salaries can’t stretch further than pay slips suggest. A simple dinner out can cost more than anticipated, and commuting expenses add up quicker than expected. Indeed, Delhi has a way of turning even a six-figure salary into a sprint to the next payday.

Rent: The Silent Bank-Breaker

Ranking among the country’s most expensive cities, Delhi rent doesn’t just take a slice of your paycheck—it devours it whole. Many young professionals find themselves living paycheck to paycheck just to cover housing costs. In this city, investing in property often seems an unattainable dream.

The Costly Social Scene

The vibrant social life of Delhi is another cost caveat. The pressure to “keep up” can lead to overspending on dining and entertainment—the hidden costs that our payslips don’t necessarily prepare us for. But who can blame you for wanting to unwind after a hectic workweek?

The Family Financial Weight Nobody Calculates

Young Indians financially stuck frequently cite their families as indirect beneficiaries of their paychecks. It’s a cultural dynamic: the parents raised you, so now you support them in return. But this responsibility adds another level of obligation to an already tight budget. While the bond is a beautiful testament to familial responsibility, its financial ramifications can’t be ignored. The emotional fulfillment of supporting family often comes at the cost of personal savings and aspirations, trapping many young Indians in a cycle where their earnings never feel their own.

The Price of Tradition

In India, the tradition of financially supporting parents is akin to a second salary, silently deducted from your account each month. This tradition, while honorable, contributes to why so many young Indians find themselves financially stuck, with dreams on hold.

Expectations vs. Reality

While young professionals expect financial independence with their first job, they quickly encounter the harsh reality of familial obligations. Balancing generosity with self-care requires tricky balancing. Achieving it is an imperative for the financially forward in our generation.

How Lifestyle Inflation Sneaks Into Indian Life

Young Indians financially stuck find themselves caught in the trap of lifestyle inflation. As incomes increase, so do expenses—not out of necessity, but out of habit, fueled by the thrill of upgrading life. What starts as a reward for hard-earned money quickly transforms into an unsustainable lifestyle. As the paychecks grow, so do the pressures to maintain an ‘Instagrammable’ lifestyle, inadvertently shrinking savings despite climbing job ladders.

From Extras to Essentials

Suddenly, a fancy smartphone, exclusive club memberships, and Uber rides become necessaries rather than occasional splurges. These additions, while initially exciting, strain finances without significant lifestyle changes.

The Illusion of Affordability

Credit cards and EMI offers instill a false sense of affordability, leading to decisions that appear sound today but become burdensome debts tomorrow. Breaking free from this cycle requires deliberate decisions to resist the allure of lifestyle inflation.

The Hidden Social Performance Tax of Urban India

Young Indians financially stuck also face an imposing, though indirect, cost: the politics of social performance. The need to appear successful in gatherings or social media often leads to unsustainable spending. A simple dinner invitation can spiral into an extravagance achieved only by swiping credit cards or digging into savings. In a city like Delhi, social status is often equated with financial worth, igniting a race to ‘keep up’ that financially constrains many young professionals.

Performing for Social Approval

The expectation to maintain a certain social appearance demands expenses on clothes, dining, travel, and lifestyles that often surpass practical limits. The bittersweet aftertaste of such indulgence is a stark reminder of overspending on fleeting approval.

Evaluating Social Priorities

It’s imperative for young professionals to reassess social expectations and refocus on authentic, valuable connections over material validations. This grounding can help break free from the financial imprisonment of fitting in.

Why Appraisals Stopped Feeling Like Wins

For young Indians financially stuck, appraisals used to be a milestone—a reasonable confirmation of growing competence and effort. Yet, in today’s economic climate, that salary hike feels more like a course correction given inflation and unrelenting expenses rather than a real reward. Increased salaries create temporary dopamine spikes, diluted promptly by skyrocketing prices of essentials and indulgences alike. What was once perceived as a victory can lose its charm under the burdens of ever-expanding costs and societal nominations.

Measurement of Real Progress

What makes “more money” meaningful is its alignment with progress. Evaluating life satisfaction through career advancements where monetary increments translate into achieving dreams rather than drowning them in existing financial commitments holds the truer measure.

The Inflation Adjustment

With inflation relentless over living standards, appraisals often compensate what should’ve been an inflated baseline all along. Many professionals encounter raised wages only to find the context recalibrating towards previous levels.

When Financial Anxiety Becomes Identity

Financial stress becomes an omnipresent shadow, morphing into identity for young Indians financially stuck, impacting mental health and well-being. It transforms from a conditional phase to permanent unrest and pressure. The pressure to excel financially transcends professional spheres, affecting mental health and self-worth profoundly. This NIH study sheds light on the far-reaching impacts of financial stress.

Understanding Financial Stress

Financial stress, exacerbated by unsustainable lifestyle choices and societal pressures, is draining. Understanding that these expectations are not worth compromising well-being is essential for young professionals looking for clarity and peace.

The Cost of Peace

Rediscovering financial equilibrium might mean scaling back choices seemingly essential but actually founded on dubious needs, fostering real connections instead. This peaceful clarity can refine identity without being chained to detrimental financial stress.

What Young Indians Are Actually Doing Differently

Young Indians financially stuck are beginning to act. They’re reclaiming fiscal strategies, leveraging technology, and prioritizing meaningful savings. Unlike preceding generations, many invest in financial literacy, seeking professional guidance, and cutting back where possible. They’re focusing on investments that reflect future needs rather than momentary pleasures, turning financial entrapment into a pursuit of freedom. Young Indians prioritize experiences and value over fleeting adornments.

Investing in Financial Literacy

The rising importance of financial literacy in India marks a generational shift. Young professionals actively engaging with online courses and advisory workshops are better equipped to navigate financial challenges strategically.

Mindful Spending

Reevaluating spending habits in favor of experiences offers fulfillment without financial hangovers. Understanding what truly adds value facilitates intelligent, conscious spending decisions unclouded by societal metrics of success.

Is This a Personal Problem or a Structural One

Young Indians financially stuck often wonder if their plight is self-created or seeded in broader structural issues. Burgeoning inflation, stagnant incomes, and cultural narratives coalesce, leaving behind a maze of challenges that exceed personal control. This perception often mutates into resignation. Yet, there exists hope—initiatives in policy advocacy and public acknowledgment of these issues promote collective spaces for addressing them. Understanding the dynamics responsible adds context to individual experiences.

Structural Challenges

India’s rapid urbanization and economic transformation introduced both opportunities and missteps. These structural challenges exacerbate the financial imbalance. Tackling them involves policy reforms aimed at housing, education, and wage growth, aligning them with evolving societal needs.

Personal Initiative

Individual actions, however, provide building blocks layer by layer for sustainable progress. Personal decisions grounded in informed actions can set a precedent that extends beyond personal fulfillment towards systemic alterations.

FAQ

Why do young Indians financially stuck despite good salaries?

Young Indians feel financially stuck often due to hidden costs and societal pressures dictating spending. Higher salaries do not account for family obligations and the desire to project social status. This expectation leads to a lifestyle inflation that diminishes savings before even realized. Therefore, despite seemingly good salaries, the financial pressure lingers persistently, challenging Indians to adapt strategies for progress.

Why is saving money so hard for Indian millennials?

For young Indians financially stuck, saving money is challenging due to lifestyle expectations, societal pressures, and family obligations, which create a demand on earnings. The desire to maintain a particular life standard often leads to increased spending, leaving little room for saving. Cultural values on familial and social contributions further blur the focus, leading to perceptions of insufficient funds to save economically.

Is the middle class in India shrinking?

The middle class in India is transforming rapidly, facing pressures from inflation and job insecurity. While its size might statistically expand, this growth may mask vulnerabilities faced by young Indians financially stuck. Economic shifts and growing disparities challenge its stability, posing questions about sustainability and the financial expectations paired with middle-class status. Understanding these changes helps identify root causes within this cohort.

How much should a young Indian professional save each month?

While savings depend on financial goals, young Indians financially stuck are advised to aim for saving 20-30% of their income monthly. Prioritizing an emergency fund and long-term goals helps mitigate unseen expenses tied to social obligations and lifestyle inflation. Starting with disciplined saving habits and employing technology aids in achieving a more structured and substantial savings outcome over time in urban contexts.

Why does cost of living in Delhi feel so high?

Delhi’s cost of living remains high due to elevated housing prices, increased utility expenses, and a bustling lifestyle that demands financial investment. Young Indians financially stuck find that basic expenses, combined with cultural entertainment, quickly swallow salaries. As Delhi evolves into a fast-paced metropolis, the equilibrium between income and cost of living remains challenging for professionals to maintain sustainably amid growing urbanization.

How do Indian family financial obligations affect savings?

Family obligations, enduring in Indian culture, significantly impact savings planning. Substantial portions of income often support family needs, expectedly and unexpectedly. This responsibility creates financial strain, leaving young Indians financially stuck as they navigate the balance between contributing to familial well-being while attempting to save against their desires for future security. Understanding these dynamics helps to pave the way for fulfilling financial requirements without depleting future reserves.

What is lifestyle inflation and why does it hit Indians harder?

Lifestyle inflation refers to rising expenses as income increases. Young Indians are financially stuck more pertinently due to societal pressure contributing to this inflation. As paychecks grow, so do material values—often blurring lines between necessity and luxury, leading to increased borrowing and fewer savings. Addressing societal narratives influencing consumption is crucial for reducing the impact of lifestyle inflation among young Indian professionals.

Why does a salary hike not improve financial stress in India?

Salary hikes often appear insufficient in improving financial stress since they merely align with increasing living costs and pressures rather than providing genuine buying power improvements. Young Indians financially stuck may witness salary boosts matched promptly by inflated expenses, negating perceived financial gain. Therefore, financial stress remains unchanged, forcing reconsideration of personal finance strategies beyond mere income increments to achieve relief.

How are young Indians managing financial pressure in 2026?

By 2026, many young Indians financially stuck have become financially literate. Exploring digital platforms and financial innovations offers layers of understanding and solutions. Adaptation includes focusing on savings, cutting unnecessary expenses, and practicing conscious consumerism. Collective awareness of cultural financial dynamics empowers Indian youth to manage emerging fiscal pressures adeptly and sustainably, emphasizing prioritization of security over material competitiveness.

Is it normal to feel financially behind despite earning well in India?

Feeling financially stuck despite earning well is increasingly common among young Indians due to multi-tiered pressures on salaries contributing to heightened financial stress. Navigating societal expectations, urban costs, and familial obligations clouds perception, breeding the constant sensation of not keeping up—even when earnings suggest otherwise. However, developing structured saving plans provides pathways for growth and security.

Conclusion

Young Indians financially stuck often find themselves on a treadmill with no stop button in sight. In my own life, I see friends and family feeling trapped in financial cycles that endanger their dreams for the future. It’s not simply a matter of altering habits, but understanding the societal, familial, and personal factors that contribute to this ongoing strain. You have the power to make changes, start saving, prioritize needs, and confront the emotions that come with the territory, thereby paving the path forward. Don’t allow these invisible second salaries to rob you of your present happiness and your future dreams.

To support this journey, consider exploring resources like this WHO guidance on mental well-being. Remember, understanding the why is your key to overcoming being financially stuck.

")